The clash between Donald Trump and Mark Carney that began in Davos — and what it could mean for the US and Canadian economies

.png "Department of Strategic Monitoring")

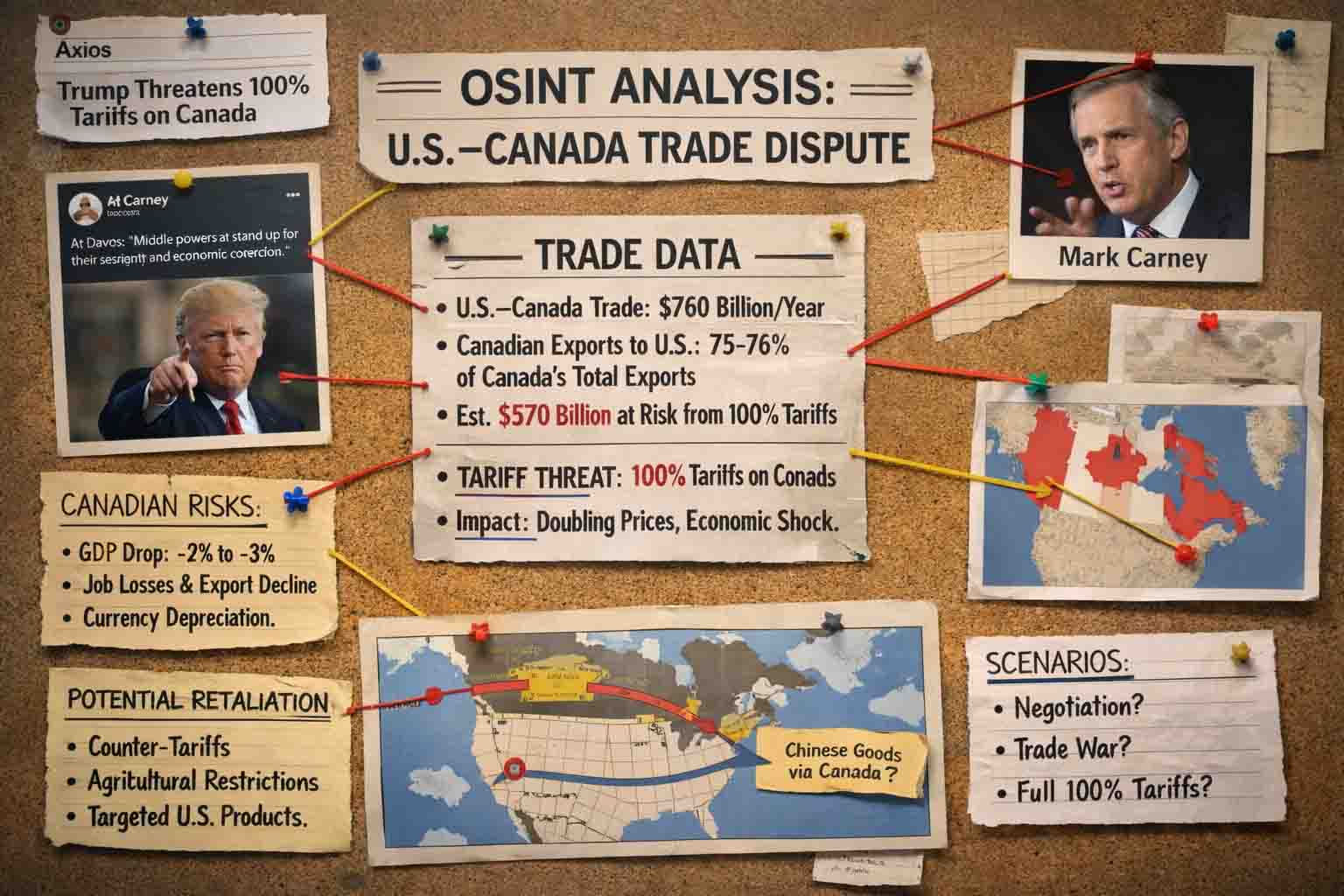

What initially looked like a routine exchange of statements on the sidelines of the Davos forum has rapidly evolved into one of the most revealing trade-political confrontations of recent months. The dispute between Donald Trump and Canadian Prime Minister Mark Carney has moved far beyond rhetoric and now threatens to turn into a serious economic stress test for two deeply interconnected economies. The core issue is not personal animosity or sharp language, but the scale of the economic levers that have been brought into play — and the hard numbers behind them.

In Davos, Carney spoke about sovereignty, the rejection of economic coercion, and the right of “middle powers” to pursue independent trade strategies in a world where rules are increasingly replaced by ultimatums. His message was framed as a systemic critique of the current global order rather than a direct attack on Washington. In the United States, however, it was received very concretely. Trump’s response evolved quickly: from dismissive rhetoric to personal remarks, and ultimately to an explicit threat — the possibility of imposing 100 % tariffs on Canadian goods.

To understand how serious such a threat is, one must look at the underlying data. In 2024–2025, total trade in goods between the United States and Canada exceeded $760 bn annually. For Canada, the US is not merely a major partner but the cornerstone of its external trade: around 75–76 % of all Canadian exports are destined for the American market. Exports as a whole account for roughly 19–20 % of Canada’s GDP, with the bulk of that share directly tied to US demand. Any major disruption of this relationship therefore translates immediately into a macroeconomic shock.

The structure of trade makes the situation even more fragile. Canadian exports to the US are dominated by energy, automobiles and auto parts, metals, and industrial machinery. Energy alone — oil and gas — represents tens, and by some estimates well over one hundred billion dollars annually. Canada remains the largest supplier of crude oil to the US, covering more than 60 % of American oil imports. The automotive sector, meanwhile, is no longer meaningfully “Canadian” or “American”: supply chains are so integrated that components may cross the border several times before a final vehicle is assembled.

Against this background, the threat of a 100 % tariff amounts to an economic rupture. In practical terms, it would double the price of Canadian goods entering the US market. In economic terms, it would wipe out the competitiveness of most Canadian exports overnight. If Canadian shipments to the US total roughly $570 bn per year, that entire volume would be at risk. Even if some firms attempted to absorb the cost through lower margins or government support, losses would still be measured in tens of billions of dollars.

For Canada, such a scenario would imply a sharp slowdown in growth and a direct hit to employment. Export-oriented industries would feel the shock first, followed by spillover effects on the labour market and investment. In a hypothetical model where 100 % tariffs are fully implemented, a drop in GDP by several points over one to two years appears entirely plausible. A weaker Canadian dollar could cushion part of the blow, but it would also fuel inflation by raising the cost of imports.

The United States, however, would not emerge unscathed. Canada is not an external supplier in the conventional sense; it is embedded within US production networks. A tariff on Canada would function as a tax on American industry itself. Automakers, energy companies, construction firms and manufacturers would face higher input costs. In sectors such as energy, where Canada dominates supply, substitution is limited in the short term, meaning higher prices would flow directly to US consumers. The result would be an inflationary impulse at odds with broader economic objectives.

Retaliation is another unavoidable dimension. Trade history suggests that countermeasures follow almost automatically. Canada has previously demonstrated its willingness to respond with targeted tariffs aimed at politically sensitive US sectors. In an escalatory scenario, American agricultural exports, consumer goods and selected industrial products would likely be hit. The combined effect could push bilateral trade down by double-digit %, with recovery taking years rather than months.

China adds a further layer to the conflict. For the Trump administration, preventing the circumvention of US trade barriers via allies is a strategic priority. Canada, in this view, risks becoming a corridor for Chinese goods and capital into North America. For Carney, expanding trade ties with China is primarily a diversification strategy — a way to reduce excessive dependence on a single market. Economic modelling suggests such diversification can offset losses, but only over time and at the cost of substantial structural adjustment.

Taken together, the numbers point to several possible paths. The most likely outcome remains tough rhetoric without full implementation, limited to selective tariffs, investigations and regulatory pressure. Under this scenario, trade volumes could fall by 5–10 %, with manageable macroeconomic damage. A harsher variant would involve a short-term shock: tariff announcements, market volatility, followed by negotiations. The most severe scenario — sustained 100 % tariffs — would amount to a dismantling of the existing North American economic model.

Ultimately, the Trump–Carney clash is not merely a personal confrontation. It is a stress test for the economic architecture linking the United States and Canada. The data make one thing clear: tariff escalation between such tightly bound economies produces mutual losses. For Canada, the risk lies in excessive reliance on a single market. For the United States, it lies in treating tariffs as a blunt political weapon while overlooking the complexity of its own supply chains. The outcome will matter not only for Ottawa and Washington, but as a signal to the entire global trading system.

Related Articles

Artificial Intelligence Enters a New Era

27 July 2026

Read more

Agentic AI: Why It Is Poised to Become the Defining Technology of the Coming Years

22 July 2026

Read more

Саммит G7 во Франции: мировые лидеры перед лицом новой эпохи глобальных вызовов

17 June 2026

Read more

China Against the System: How Beijing Is Preparing for an Era of Great Global Confrontation

23 May 2026

Read more